🎯 TUESDAY TARGET: Bristol-Myers Squibb (BMY) | 👇 Reveal the Play

🧠 NEW: Elite Trader Plan. A calm, step-by-step options roadmap to grow your account and tame big swings | 👇 Jump to Details

AI tickers get the blame because they are loud. The real story has been whispering in the funding markets. When the overnight rate for secured cash (SOFR) pushed above what banks earn by leaving money at the Fed (IORB), the incentive shifted: park cash, don’t lend it. That tiny spread did the heavy lifting. Repo lines tightened, funding costs jumped, and the fastest‑money cohort trimmed exposure. High‑beta clusters, AI, crypto, momentum, didn’t “fall out of favor”; they lost cheap leverage.

Think of SOFR as the price of overnight oxygen for hedge funds and basis traders. A higher price means smaller lungs. Less leverage means smaller positions. Smaller positions mean weaker bids under the names everyone thought were bulletproof. That’s why you felt the wobble first in the same places that rallied hardest.

Now zoom out from the tick‑by‑tick: the government is open, Treasury’s cash pile will be spent, and balance‑sheet runoff is nearing its late innings. All three add reserves back into the system. As those dollars re‑enter the plumbing, SOFR tends to drift back toward the policy rate, repo haircuts ease, and counterparties loosen lines. Liquidity repairs sentiment long before narratives do.

Everyone will watch one company’s guidance. We’ll watch whether the price of leverage is backing off. When the pipes breathe easier, the pixels usually recover on their own.

Below, as always, the rest of what’s cooking:

The AI Credit Signal Fired First

Credit sniffed the shift before equities. Amazon’s USD deal was upsized to $15B, extending a hyperscaler issuance wave that pushed spreads wider and CDS on key names higher (Oracle ~105bp at the wides). A wrinkle: Saba reportedly sold protection to banks seeking hedges on big tech, providing a short‑term counter‑signal.

The Fed’s Message: Insurance, Patience, and Data Gaps

Governor Waller reiterated preference for a 25bp December cut as “labor near stall speed,” while Vice Chair Jefferson stressed moving carefully near neutral. Fed minutes sit between a liquidity squeeze and a data backlog, with market odds of a December cut slipping <40%. The policy mix remains supportive, but the curve will take its cue from jobs and core inflation in coming prints.

Rare‑Earth “Truce”: Stuck in the Queue

Washington framed China’s general licenses as a meaningful opening for rare earths and allied critical minerals. Weeks later, exporters report little practical change and licenses can still be used as leverage. For semis, EV, and defense value chains, this keeps the procurement premium in place and complicates “de‑risked” reshoring timelines.

Single‑Stock Gravity: NVDA Still Sets the Weather

NVDA’s realized volatility exceeded the average Russell 2000 name; a reminder of its outsized weight in index mechanics and how quickly factor P&L can move around a single print. Add VIX expiry Wednesday, NVDA earnings Wednesday night, and monthly OpEx Friday: a cluster that can compress implied vol then expand realized vol on contact.

The Week: Minutes, Jobs, and a Volatility Cluster

Macro returns with a dense tape: FOMC minutes Wednesday (2pm ET), Nvidia after the close, and VIX expiry Wednesday morning into monthly OpEx Friday. The delayed September payrolls land Thursday (street clustering around +50–80k; unemployment ~4.3%), alongside claims and the Philadelphia Fed; 20‑yr supply hits Wednesday and 10‑yr TIPS Thursday. Retail heavyweights (WMT, HD, TGT, TJX, LOW) report through mid‑week, while flash PMIs and Michigan wrap Friday. Fed speakers are scattered across the week, but the market focus is squarely on whether minutes plus payrolls re‑price December odds, and how NVDA’s print steers factor risk into OpEx.

Tactics for this Tape

Consider replacing some tech delta with options; keep a watchlist of cash‑rich AI beneficiaries with improving free cash flow, not just “adjusted” stories. Rotation: maintain a bid for quality defensives while the liquidity toggle resolves.

Get Rich Overnight with Options? Yeah Right...

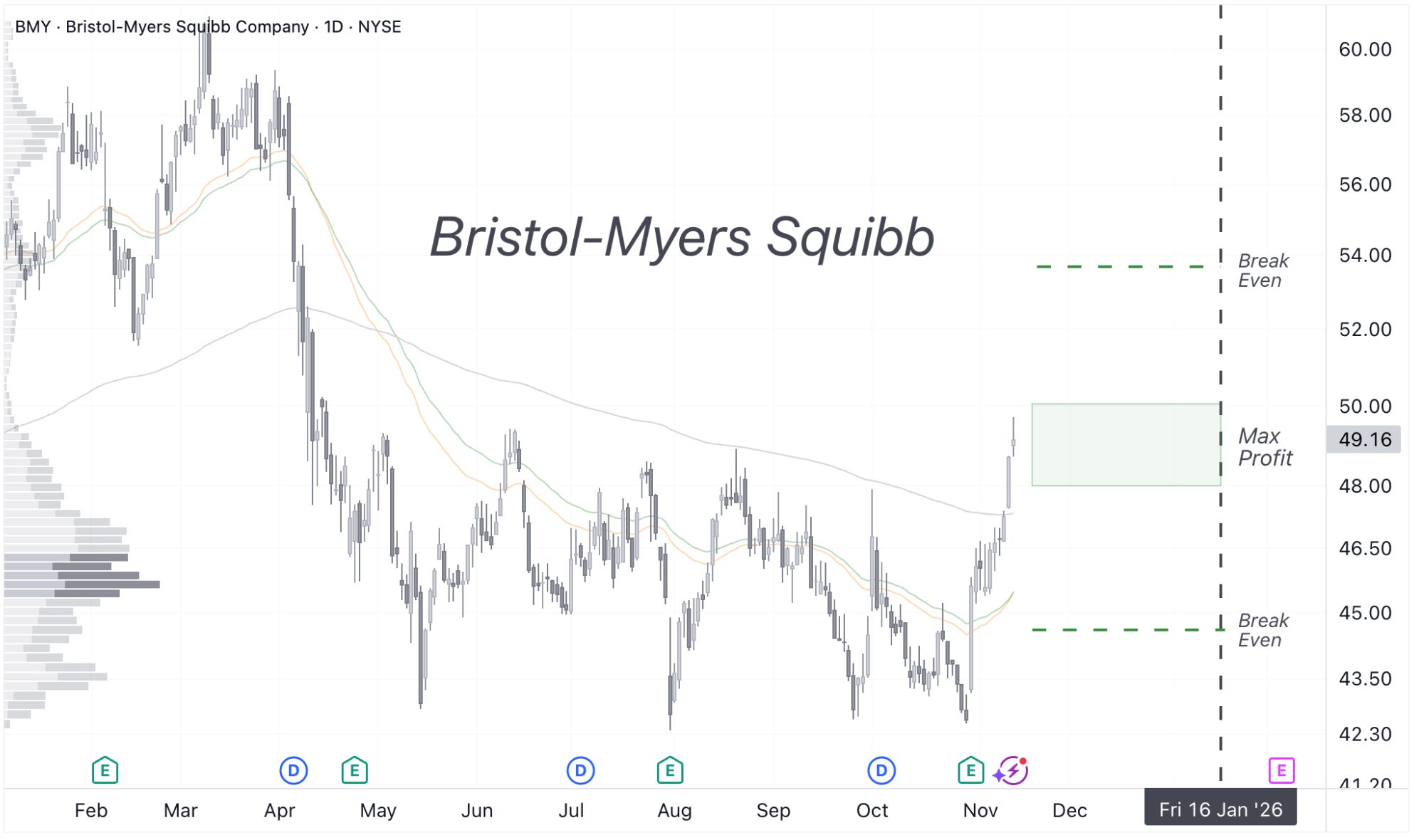

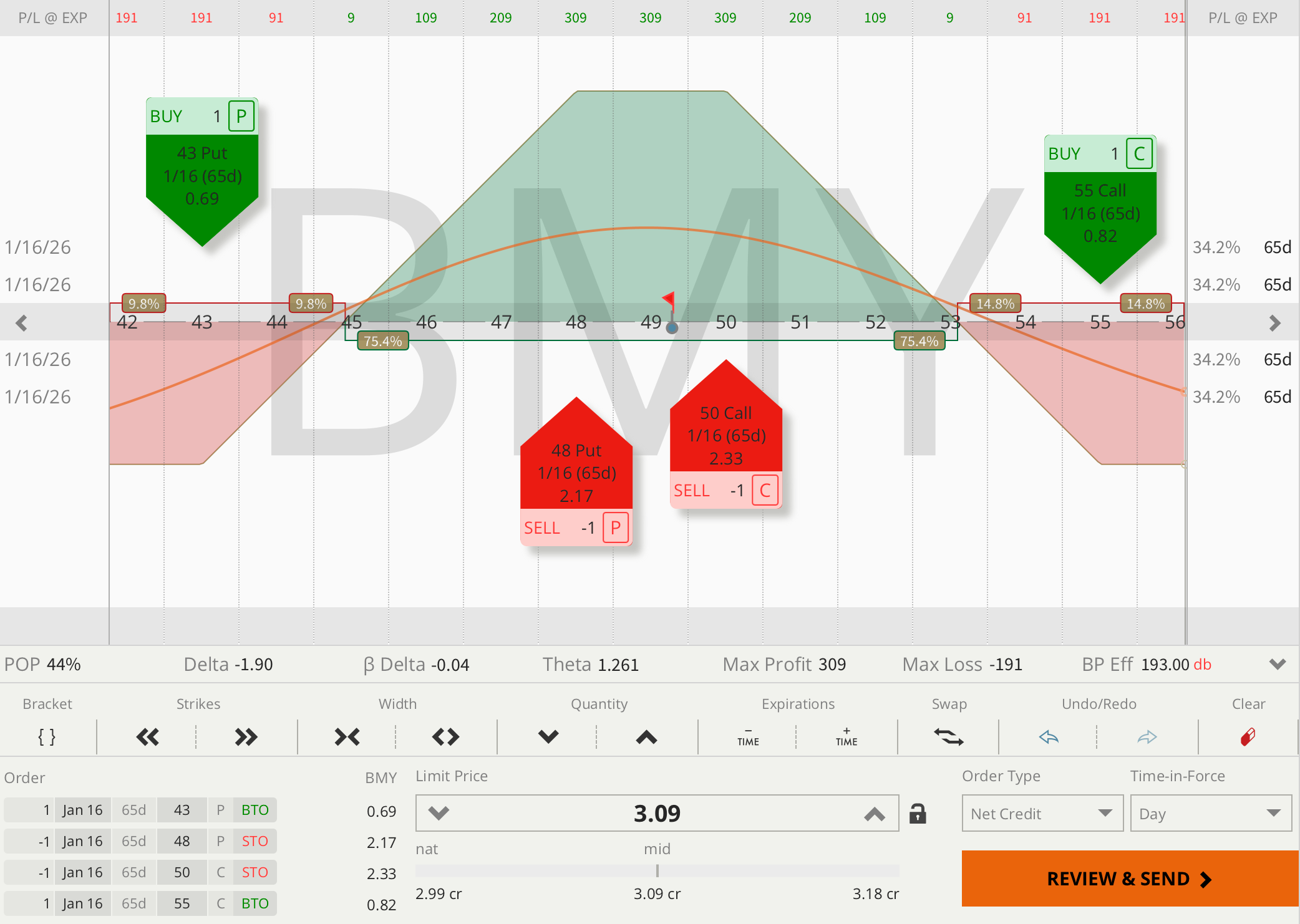

TUESDAY TARGET: Bristol-Myers Squibb (BMY)

We entered this trade a few sessions ago, but the thesis hasn’t shifted; if anything, the recent pullback offers a better entry.

The setup still looks like a classic case of “trying to break out, but not yet supported by strong fundamentals.” What we do like: the 40- and 50-day moving averages are crossing, and the 200-day is starting to turn upward; an early hint of a potential trend change.

All our recent trades and the reasoning behind them can be found in the Trade Alerts section. Think of it as a behind-the-scenes look into our process, so you can decide if it’s worth adopting (or adapting) in your own strategy.

🧠 Elite Trader Plan

And if you need a calm, step-by-step options plan that grows accounts and tames big swings, check out the Elite Trader Plan. In 4–8 sessions, I’ll bring you fully up to speed, all included in the plan.

📅 Regular Mentorship Call

More time = more value.

📌 Advanced Options

📌 Risk Management

📌 Capital Efficiency

Rate: $135 | 👉 Book 60-Minute Call

Elite Trader: $110 | 👉 Book Elite Trader Call

⏳ 30-Minute Session

Less time = more often.

📚 In-Depth Learning

🧠 Strategy Breakdowns

🔍 Trade Reviews

Rate: $75 | 👉 Book 30-Minute Call

Elite Trader: $55 | 👉 Book Elite Trader Call

Tuesday Target is written by Juri von Randow — founder of MacroDozer, professional investor, and trading mentor — delivering institutional-grade trade ideas, market insights, and strategy every week for serious investors.

🚨 Educational content only. Not financial advice. Past performance ≠ future results.